Inventory Takes Center Stage as Foreclosures Fade

(Source: Wall Street Journal) – If real estate trends were animals in the Chinese lunar calendar, last year might have been called the “Year of the Disappearing REO.” If real estate data-provider CoreLogic CLGX -2.35% is right, this year will be the “Year of the Tight Inventory.”

Last week, the Journal reported that U.S. home prices are on track to post a yearly gain for the first time since 2006, according to one closely watched national price index.

Behind these price gains—which come as good news to millions of homeowners  counting on the value of their houses to carry them into retirement, or those looking to sell or borrow against their homes—is rising demand. Investors, first-time homeowners and move-up buyers alike are all re-entering the market as the economy slowly improves and interest rates remain low.

counting on the value of their houses to carry them into retirement, or those looking to sell or borrow against their homes—is rising demand. Investors, first-time homeowners and move-up buyers alike are all re-entering the market as the economy slowly improves and interest rates remain low.

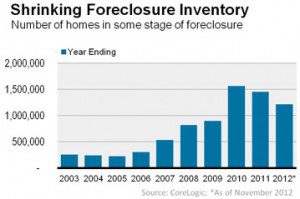

But another reason prices are climbing is that foreclosures are becoming less relevant in the market. CoreLogic reports that about 1.2 million homes, or 3% of all U.S. homes that have a mortgage, were in some stage of the foreclosure process as of November. This figure, known as the foreclosure inventory, is down 20% from a year ago, when 1.5 million, or 3.5% of all mortgaged homes in the country, were going through the foreclosure process.

Also down is the share of home sales that come from what is known as real estate-owned properties, or REO, which refer to homes that have been repossessed by banks through the foreclosure process. According to CoreLogic, the REO share fell from 19.6% to 11.5% between January and November of 2012. To wit: banks are selling fewer repossessed homes, which means less competition for sellers who are not in foreclosure, and eventually, rising prices.

There are two main reasons that the REO share, and foreclosures, are down. First, of course, is that delinquencies are down: LPS Applied Analytics reported last month that the mortgage delinquency rate fell from 7.83% to 7.12% between November 2011 and November 2012.

There are two main reasons that the REO share, and foreclosures, are down. First, of course, is that delinquencies are down: LPS Applied Analytics reported last month that the mortgage delinquency rate fell from 7.83% to 7.12% between November 2011 and November 2012.

But more significantly, the foreclosure process has become longer and more arduous, chiefly in states where it is handled by courts. Banks slowed foreclosures after the “robo-signing” scandal emerged two years ago, revealing widespread abuses and sloppy practices in processing legal paperwork related to seizing homes with delinquent mortgages, and began to focus more on short sales and mortgage modifications. A slower foreclosure process and more short sales and loan mods has meant, over the last year, that fewer properties make it all the way through the foreclosure pipeline to REO status.

But the decline in REO share will be less dramatic in 2013, says Sam Khater, CoreLogic’s senior economist. That’s because in non-judicial states like California, Arizona and Nevada, where foreclosures are not always handled by the courts, the foreclosure pipeline has cleared much faster than in judicial states such as Florida, New York and New Jersey.

“The foreclosure crisis has shifted east, to the judicial states, where the pipeline is slow,” Mr. Khater said in an interview Thursday, and the pace at which delinquent loans become REO properties has settled at a fairly slow clip. “The big driver in 2012 in prices increases was the decline in REOs, but I think the big move-down has already happened. The driving prices in 2013 will be the tighter inventory.”